Stablecoins Are Just the Beginning: Mapping the Tokenized Asset Opportunity

Stablecoins proved that onchain money works.

The numbers are undeniable. Stablecoins represent roughly $300 billion in circulating supply, process about $10 trillion in monthly transfer volume, and are used by more than 54 million monthly active addresses.

Stablecoins demonstrated that blockchain networks can support real economic activity at scale. Value moves globally and settles continuously, financial instruments exist as programmable digital assets, and users hold and transfer these assets directly through digital wallets. Stablecoins succeeded because they solved real economic problems: fast global settlement and easier access to digital dollars.

If stablecoins were the first major financial primitive to successfully move onchain, the natural question is: What comes next?

Many builders and executives believe that the next phase of blockchain adoption involves tokenizing real-world assets (RWAs). These include financial instruments such as credit, funds, equities, and commodities represented as digital tokens on blockchain networks.

But tokenization is a tool, not an end in itself.

Not every asset benefits from being onchain. In many cases, existing financial infrastructure already works extremely well. The key question, therefore, is not whether assets will be tokenized, but where tokenization creates meaningful economic value.

This is a timely matter to discuss because regulatory frameworks are taking shape globally, and clarity around tokenization is more present now than ever. The market is adopting this infrastructure at an accelerated pace. This piece reflects my current attempt to map that landscape. It outlines how I think about the structural models behind tokenized assets, highlights where early adoption is emerging, and points to areas where I see new financial markets developing as tokenized assets become programmable collateral within onchain financial systems.

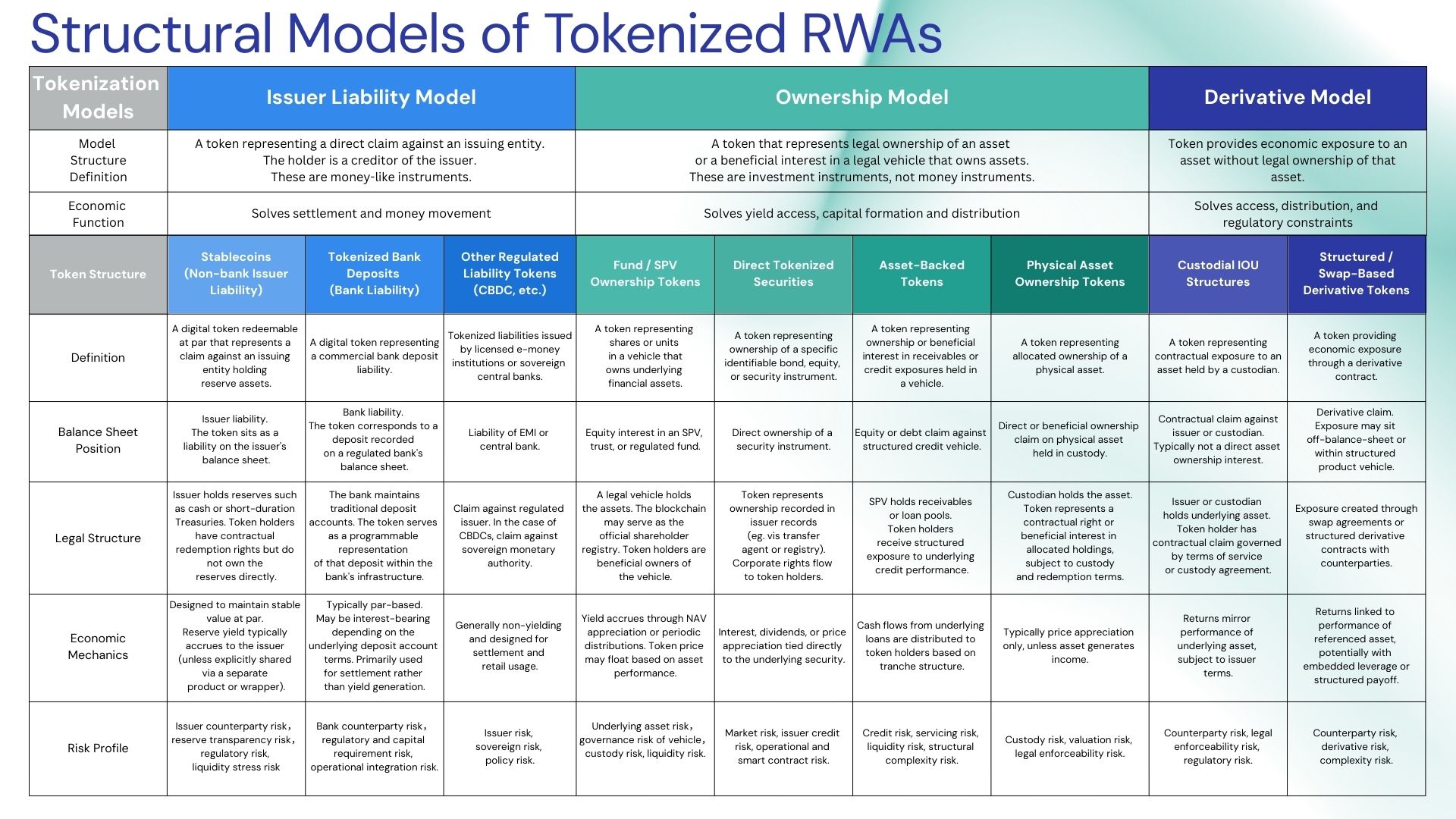

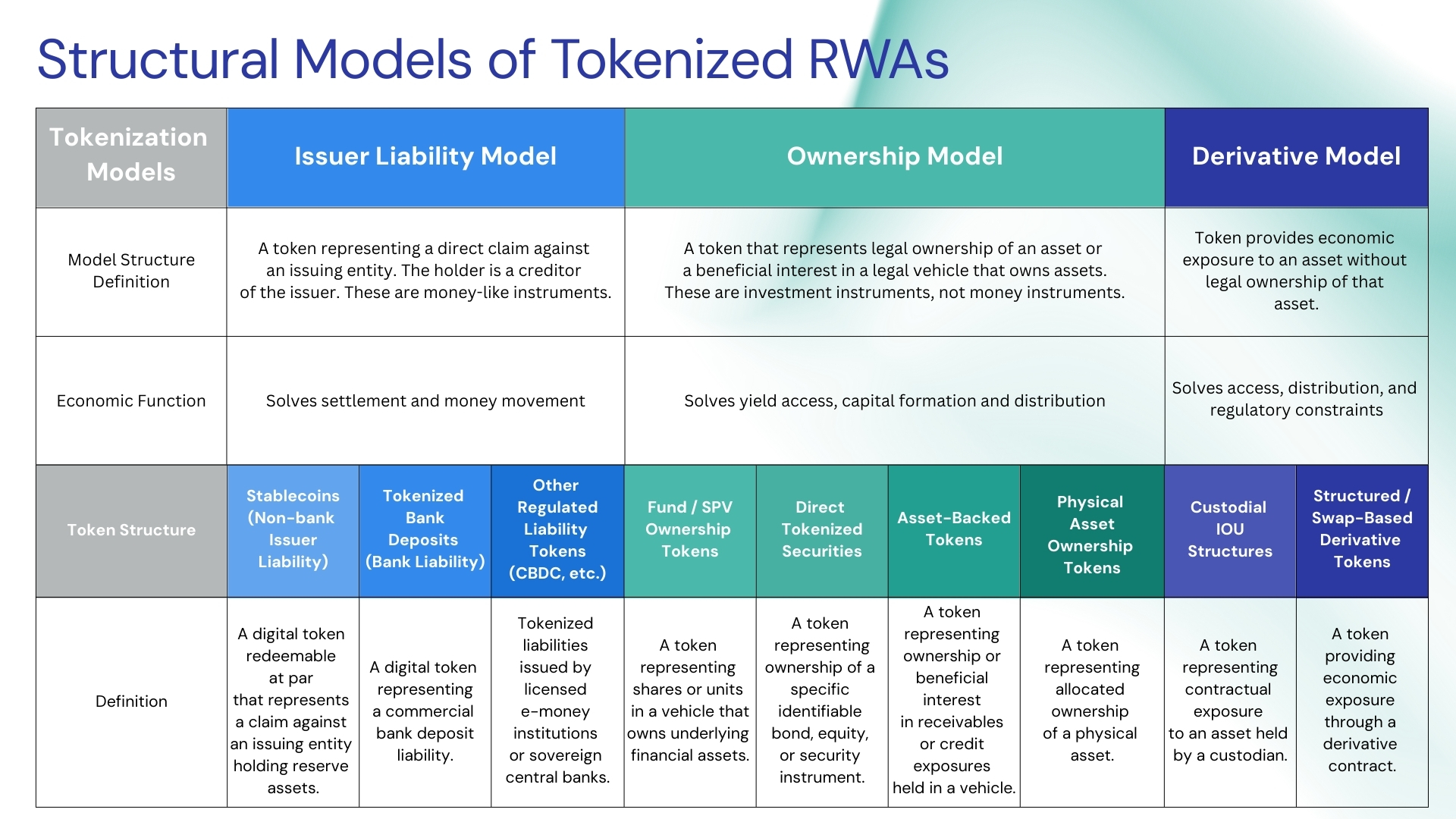

Understanding the Structural Models of Tokenized Assets

Before we discuss the impact of tokenization, we need to define the market’s structure. One of the most confusing aspects of the tokenized RWA ecosystem is that the term “tokenization” is often used to describe very different financial structures.

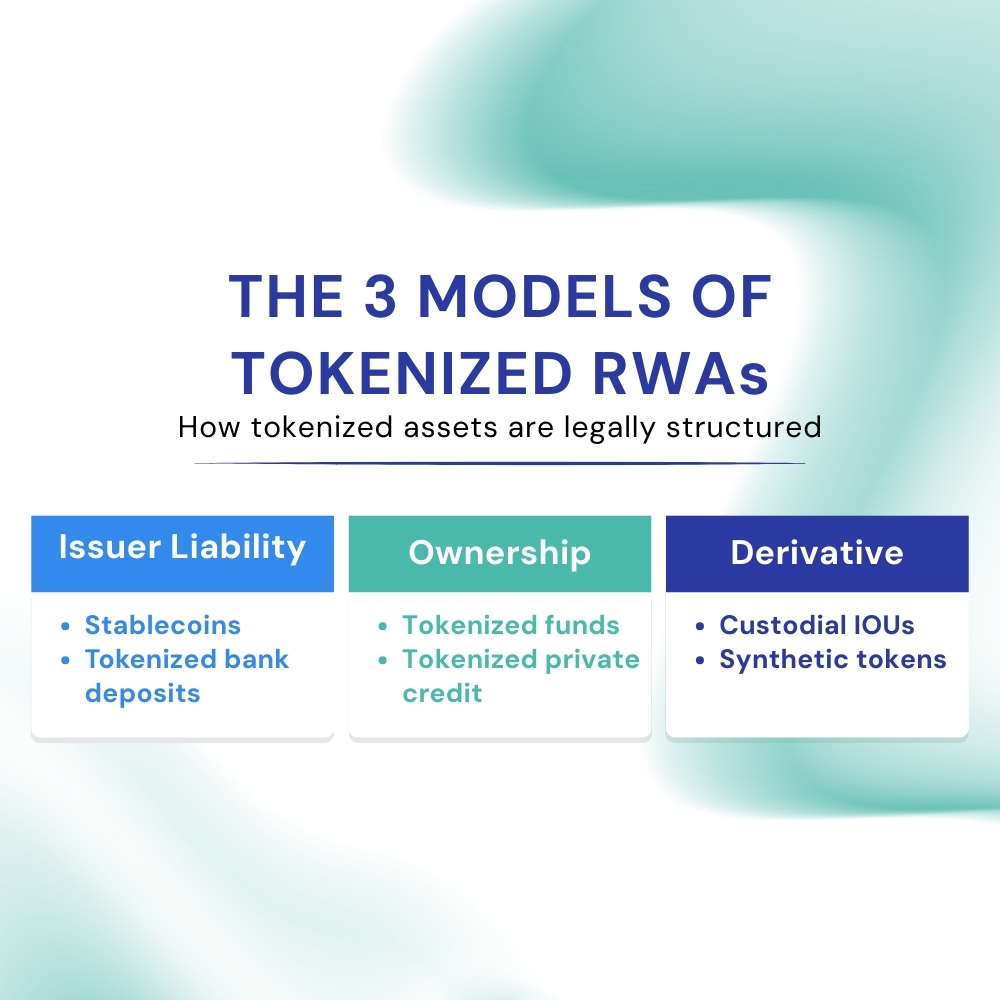

Tokens may appear similar onchain but represent fundamentally different legal rights. In thinking about this reality, I have developed a framework of three distinct Tokenization Models:

- Issuer Liability Model: represents a liability issued by an institution, similar to money (ex. Stablecoins)

- Ownership Model: represents direct ownership of an underlying asset (ex. Tokenized treasury fund)

- Derivative Model: provides economic exposure through a derivative structure (ex. Tokenized synthetic public equity)

These distinctions determine what a token holder actually owns and how risk is allocated across the system.

Because many stablecoins hold U.S. Treasuries as reserve assets, they are sometimes loosely described as “tokenized Treasuries.” In reality, they are something quite different. Stablecoins represent issuer liabilities backed by reserve assets such as cash or short-duration Treasuries. Token holders do not own those Treasuries directly. Instead, they hold a claim against the issuer.

By contrast, tokenized Treasury funds represent direct ownership interests in a vehicle that holds government securities. The token in that case is not money. Rather, it is an investment instrument.

A third structure involves derivative exposure. In these models, the token does not represent ownership of the underlying asset at all, but rather a contractual exposure to its price or performance. Some recent tokenized equity products follow this approach, in which the token tracks the value of a public stock but does not provide the holder with shareholder rights such as voting or direct ownership of the underlying shares.

Understanding these structural differences is essential for evaluating both the opportunities and the risks in the tokenized RWA ecosystem. The framework below summarizes the three primary Tokenization Models and the token structures that typically fall within each category. Additional structural details are included in the appendix for readers interested in the underlying legal and balance-sheet mechanics.

Why Tokenization Matters Economically

Tokenization is often framed as a technological shift, but what ultimately matters is its economic impact. Tokenization does not benefit every asset class equally.

Many financial markets already operate with deep liquidity, efficient settlement systems, and well-established legal frameworks. Public equity markets, for example, already provide global access and high liquidity, raising an open question about how much incremental value tokenization ultimately adds.

The same logic applies to tokenized RWAs. Any asset can be tokenized. The key question is where tokenization creates meaningful value.

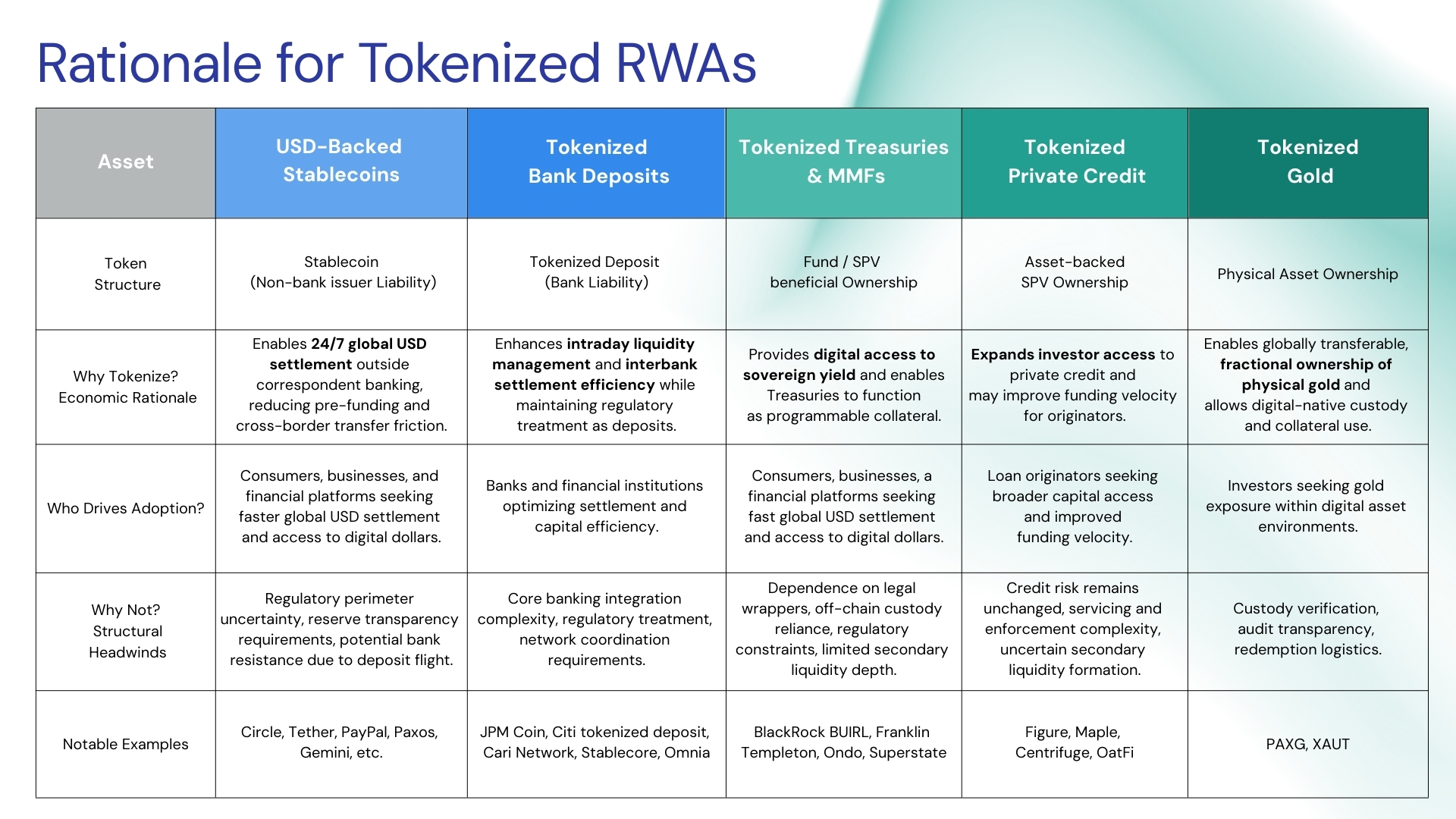

With that lens in mind, the table below summarizes several asset classes currently being explored in the tokenized RWA ecosystem.

Where Early Signals Are Emerging

While tokenized RWAs remain early, the growth trajectory is impressive. Excluding stablecoins, there are approximately $26 billion in distributed tokenized RWAs outstanding as of March 1, 2026, compared to roughly $6.7 billion one year earlier, representing nearly 4x YoY growth. The market appears significantly larger when including represented RWAs, where blockchains are used primarily as a recordkeeping layer rather than as a distribution layer. In these structures, the blockchain improves transparency, reconciliation, and operational efficiency, but investors do not hold the assets directly onchain. Including those represented structures, the broader universe of blockchain-recorded RWAs approaches roughly $390 billion, driven largely by repurchase agreement markets.

Tokenization represents only basis points of the global financial markets, but the growth rate suggests the infrastructure is beginning to support real economic activity across multiple asset classes.

A few areas show particularly meaningful early traction that I am excited about.

Tokenized Private Credit

Private credit looks particularly compatible with tokenized distribution models because these markets already rely on structured vehicles, private capital networks, and relatively illiquid instruments. Tokenization can expand investor access while improving capital formation for originators. Tokenized private credit represents roughly $22 billion when including both distributed and represented RWAs, making it one of the largest tokenized asset categories today. Companies such as Figure, Maple, and Centrifuge are already demonstrating how credit origination, securitization, and distribution can occur directly through tokenized infrastructure.

Tokenized Deposits

Tokenized deposits are an effort by regulated banks to bring traditional deposit liabilities into blockchain-based settlement systems. Unlike stablecoins, which are issued by private companies and compete with bank deposits, tokenized deposits allow banks to represent customer deposits as digital tokens while keeping those liabilities inside the banking system. This allows banks to participate in emerging onchain financial infrastructure without losing deposit liabilities to external stablecoin issuers. It also creates the potential for faster interbank settlement and more capital-efficient liquidity movement across financial institutions. Initiatives such as Cari Network, along with infrastructure companies including Stablecore and Omnia, are building systems designed to enable interoperable settlement between financial institutions through tokenized deposits.

Onchain Collateralized Credit

A second-order effect of tokenized assets may be the emergence of entirely new credit markets built on top of tokenized collateral. Protocols such as Aave and Morpho already allow users to borrow against digital assets within fully onchain lending systems. As more financial assets become tokenized, similar mechanisms could allow investors to borrow against tokenized treasuries, credit instruments, or other financial assets. In this sense, onchain collateralized credit is not itself a tokenized RWA, but rather a new financial primitive made possible by tokenized infrastructure. Personally, this is one of the aspects of tokenization that I find most exciting. Once financial assets exist as programmable collateral, entirely new credit markets and financial structures become possible, many of which likely have not yet been imagined.

An Invitation to Builders

While the volume of RWA tokenization remains small relative to traditional markets and structural questions remain, the directional trend is clear. Stablecoins demonstrated that a financial primitive can migrate onchain and find product-market fit. Tokenized RWAs represent the next stage of that evolution, though not all assets will move at the same pace or for the same reasons.

What is most compelling is not simply the digitization of existing instruments, but the possibility of rebuilding certain layers of financial infrastructure in ways that are legally grounded, operationally efficient, and interoperable with digital-native capital. There is still much to learn.

If you are building in this space, particularly around tokenized deposits, private credit infrastructure, issuance platforms, digital collateral markets, or the infrastructure that makes this all possible, I would welcome the conversation. Feel free to reach out at [email protected]